9 Jun 2026

Why Your Payments Are Failing And What's Really Happening Behind That Loading Screen

Ever wondered what really happens when a shopper clicks 'Buy'? And why does the payment sometimes just... fail?

Despite all the recent innovations in fintech, failed payments remain a massive and expensive hurdle – one that doesn't get nearly enough attention.

According to industry reports, 15–20% of online transactions initially fail. This aligns with what major players like Adyen, Mastercard, and Visa have publicly communicated (an average authorization rate of around 85% for card-not-present (CNP) transactions).

But that's just the global average. In emerging markets, the picture is even more stark. At NjiaPay, we've worked with clients where up to 30% of their online payments were failing, yikes.

So, what exactly is happening during that loading screen? Let's break it down.

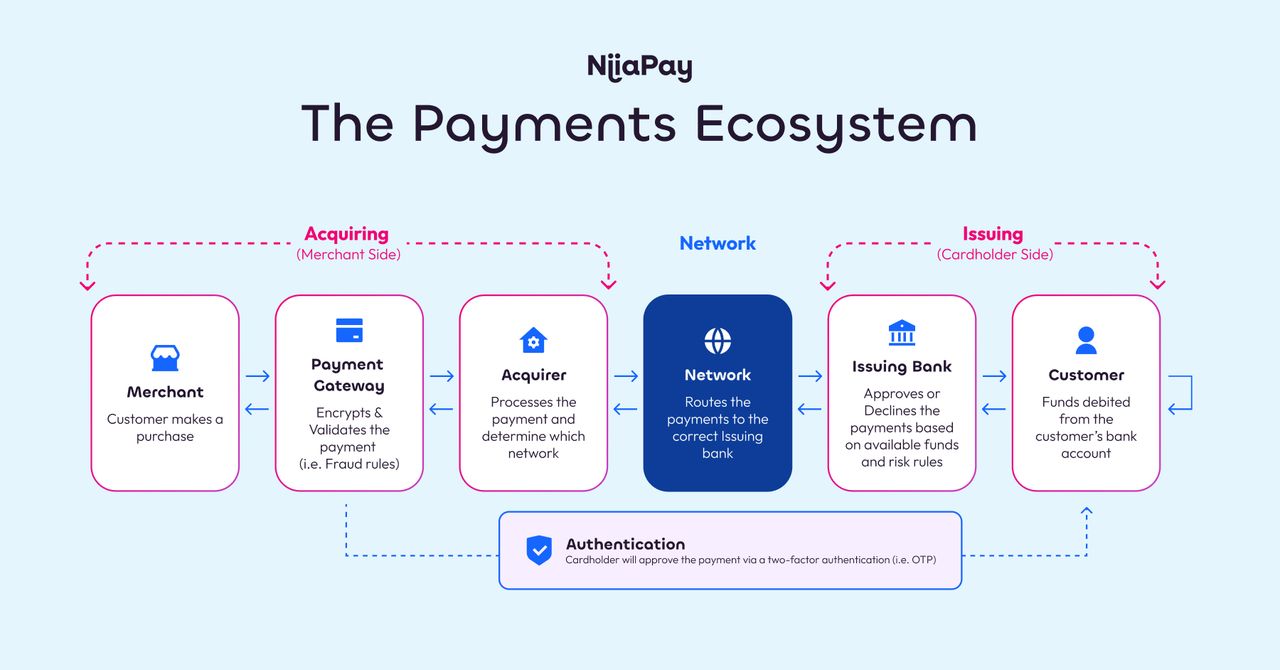

The Millisecond Journey Your Payment Takes

When a customer hits 'Pay', the transaction embarks on a complex journey through a highly fragmented value chain, all in a matter of seconds. Here's what that looks like:

1. Payment Gateway The gateway captures and encrypts the payment data, assigns a fraud risk score, and routes the transaction; either to a 3DS authentication provider (which is a digital security checkpoint) or directly to the processor.

2. Payment Processor & Acquirer The processor sends your transaction and packages it alongside over 100 different data points (things like country, currency, merchant category code, device type, and transaction history) before sending it off to the relevant card networks. The richer this data bundle, the more confident the issuing bank feels approving the payment.

3. Card Networks (Schemes) Think Visa, Mastercard, or similar. They act as the middleman connecting the merchant's bank to the customer's bank, and communicate what type of transaction is being processed.

4. Issuing Bank Finally, the customer's own bank analyses the request. It checks for available funds, runs its own fraud algorithms (whether 3DS or non-3DS), and makes the ultimate call: approve or decline.

That's four distinct layers. And in practice, there can be five or more separate systems all relying on each other to work in perfect harmony.

The Core Problem: Infrastructure Fragmentation

Here's where things start to fall apart.

Each "hop" in this value chain introduces a new point of failure. It also means a loss of valuable data that the issuing bank would otherwise use to determine whether a payment is legitimate.

Differences in risk appetite between providers, competing security protocols, legacy network downtime, or even a misconfigured API between two distinct systems: any one of these can instantly trigger a decline.

A payment stack built on outdated infrastructure, patched together with multiple third-party systems, will always have cracks. Not because any one provider is failing, but because the more handoffs there are, the more chances there are for something to go wrong.

The Solution: Fewer Hops, Higher Success Rates

The logic is simple: fewer hops = fewer points of failure = higher authorisation rates.

This isn't theoretical. Seeing it firsthand at Adyen was an eye-opener. By owning the end-to-end flow, the improvements were tangible. Better latency, faster product innovation, and meaningfully higher auth rates.

This is also why more businesses are exploring alternative ways to move money altogether. Rather than routing a payment through the traditional card network (gateway, processor, scheme, bank) newer rails like account-to-account transfers and digital wallets create a far shorter path. By taking a more direct route, modern solutions cut out several intermediaries entirely. The result? Less friction, fewer points of failure, and money moving more reliably from the shopper's bank to the merchant.

At NjiaPay, this thinking sits at the heart of what we're building. In markets where fragmentation is greatest, the opportunity to streamline the flow, and recapture that lost revenue – is enormous.

What This Means for Your Business

If you're an online merchant, payment failure data is one of the most valuable and underutilised signals available to you. A few questions worth asking:

- Do you know your current authorisation rate by market, device, and payment method?

- Can you identify where in the chain your declines are happening?

- Are you working with a consolidated payment stack, or are you adding intermediaries with every new market you enter?

The difference between an 85% and a 95% authorisation rate isn't just a number; it's revenue that's either reaching you or evaporating into thin air.

Interested in understanding how NjiaPay helps businesses in emerging markets like South Africa reduce payment failures and increase authorisation rates? Get in touch →